EV Battery Longevity Is Delaying the Feedstock Wave

Longer-lived EVs are pushing true retirement feedstock later, even as crash-sourced battery inventories grow than replacement and second-life demand.

Need to identify the pack before you route it?

Use Explorer to connect VIN context, pack identity, label evidence, chemistry, fitment, and lifecycle routing context before pricing, listing, reusing, or recycling a battery.

Longer-lasting EV batteries are good news for vehicle owners. They are more complicated news for salvage yards, second-life buyers, remanufacturers, and recyclers.

Recent Wall Street Journal reporting framed the consumer story clearly: modern EV batteries are retaining useful range after heavy mileage, and buyer perception has not caught up. That is true, but it is not the whole market story.

For battery lifecycle operators, durability is only the first delay. The vehicle may remain in service for years, move through a warranty channel, or leave the country with its battery still installed. At the same time, crash-sourced packs can accumulate in salvage inventory when replacement and second-life demand is thin. The result is not simple scarcity. It is a mismatch between the batteries available today and the feedstock, timing, location, and condition each buyer needs.

Quick answer

EV battery longevity is delaying true aged-retirement feedstock, not every form of used-pack supply. Battery replacements remain rare, vehicles stay in service longer, warranties keep covered failures in OEM channels, and exports move batteries out of domestic collection systems. Meanwhile, crash-sourced packs can build up faster than repair and second-life buyers absorb them. For operators, the issue is not only volume. It is timing, geography, identity, condition, and buyer fit.

Key Takeaways

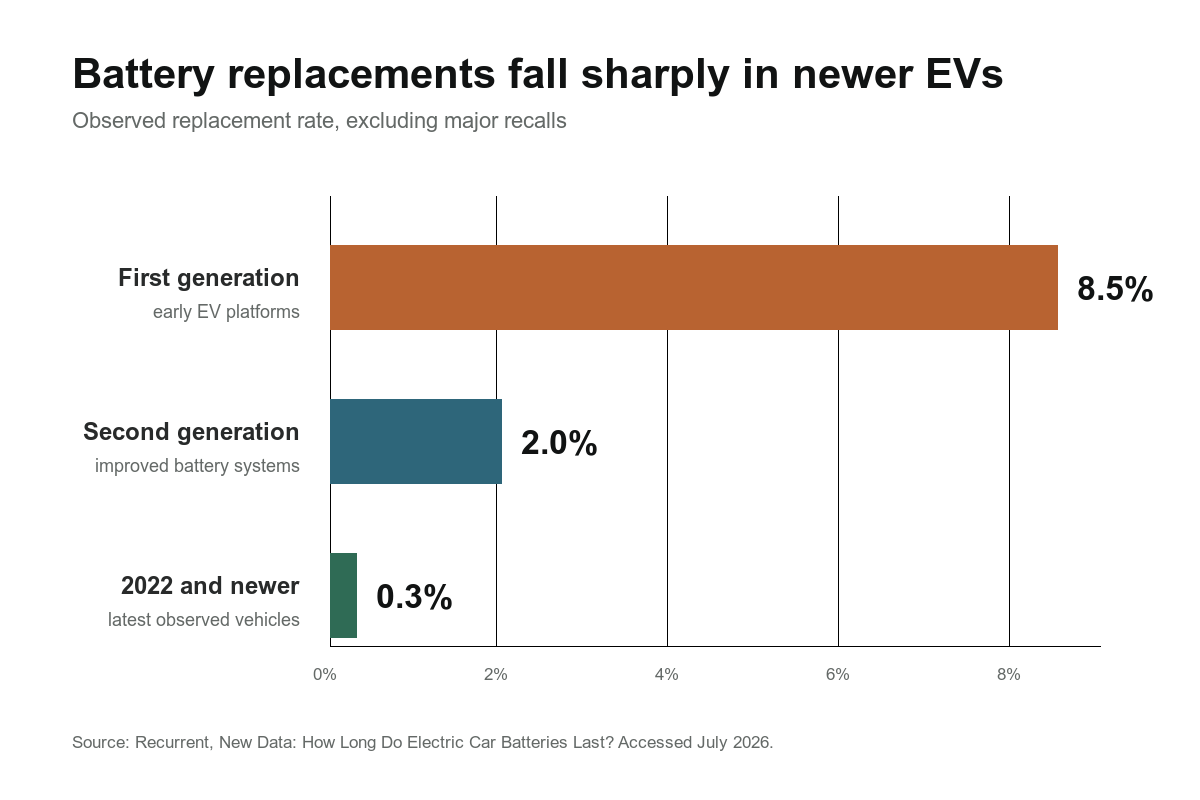

- Modern EV battery replacements are still uncommon outside major recalls. Recurrent's 2025 analysis found fewer than 4% of EVs across all years and models had battery replacements outside major recalls, with 2022-and-newer EVs at 0.3%.

- Feedstock forecasts have to follow the vehicle cohort, not a fixed battery retirement age. More than half of EV batteries may remain in their original applications beyond year 17.

- Exports are a major feedstock leak. Roughly 40% of EVs placed on the U.S. market may ultimately be exported with their batteries still inside.

- Slow aged retirements and growing salvage inventories can coexist. Observed used-pack prices are falling because many one-off packs do not match enough replacement or repurposing demand.

- Second-life buyers need repeatable pack families, known condition, and a cost advantage after testing, integration, certification, warranty, and support.

- For recyclers, feedstock access and plant utilization matter as much as nameplate capacity. High fixed costs do not disappear because a facility was built early.

What EV Battery Longevity Means For Salvage Yards

The headline sounds simple: EV batteries are lasting longer than expected. For a salvage yard, that does not automatically mean every used EV pack becomes more valuable or easier to sell.

It means the first sorting question changes.

Before asking "what is the used battery worth?", the operator has to ask:

- Is the vehicle still inside battery warranty coverage?

- Was the pack replaced, recalled, damaged, or removed?

- Is the battery available because of age, collision, flood, theft recovery, fleet retirement, or a service event?

- Can the pack be identified from the VIN, physical labels, part numbers, and photos?

- Is state of health known, estimated, or unknown?

- Is the buyer a repair customer, remanufacturer, second-life operator, recycler, or core buyer?

Those questions matter because a warranty-age battery failure is not the same kind of supply as an out-of-warranty salvage pack. A covered owner with a failed high-voltage battery is much more likely to go through the dealer or manufacturer for a covered repair. That replacement battery does not normally become open-market used inventory for the independent salvage channel.

The practical salvage opportunity is more likely to come from vehicles and packs that fall outside that simple consumer warranty path: high-mileage commercial use, taxis, rideshare, delivery fleets, crash-total-loss vehicles, old first-generation EVs, loose packs, and battery families with known buyer demand.

Pack identification is a market function, not just a catalog lookup. A salvage team needs to identify EV battery packs by VIN and labels, reconcile the EV battery pack part number, document condition, and route the pack based on evidence.

Battery Longevity Is Pushing The Replacement Curve Later

The strongest available data points in the research all point in the same direction: the mass consumer EV battery replacement wave is arriving later than many expected.

Recurrent's 2025 battery replacement analysis found that, outside major recalls, fewer than 4% of EVs across all years and models had battery replacements. The rate was much higher for first-generation EVs at about 8.5%, lower for second-generation EVs at about 2%, and very low for 2022-and-newer EVs at 0.3%.

Geotab's EV battery health work also supports a longer useful-life curve. Its fleet analysis found average battery degradation of 2.3% per year. At that pace, the average battery would still retain roughly 81.6% state of health after eight years.

Stanford and SLAC researchers found another important point for lifecycle planning: real-world driving patterns can make batteries last about one-third to 40% longer than conventional lab cycling assumptions suggested.

The business implication is straightforward. If battery replacements are rare, and if degradation is slower than expected, then a market model built around early age-based pack failures will overestimate near-term used-pack and recycling supply.

The Vehicle, Not Just The Battery, Determines Feedstock Timing

A battery does not become domestic recycling feedstock simply because it reaches a modeled age. It normally remains inside a vehicle until a warranty event, collision, dismantling decision, export, or true vehicle retirement changes its route.

Circular Energy Storage's lifecycle research says more than half of EV batteries placed on the market remain in their original applications beyond year 17. Its U.S. cohort forecasts also indicate that roughly 40% of EVs will ultimately be exported, carrying their batteries into another market. Those two factors can move meaningful domestic feedstock much further out than a simple 8-, 10-, or 15-year retirement assumption.

| Lifecycle event | What happens to supply | Planning implication |

|---|---|---|

| Battery replacement | A pack leaves a vehicle because of failure, degradation, recall, or service action. | Replacement rates help explain service supply, but not the full retirement curve. |

| Vehicle retirement | The pack may become available for reuse, resale, repurposing, or recycling. | Vehicle survival is the better starting point for aged-feedstock forecasts. |

| Whole-vehicle export | The battery remains in use but leaves the domestic collection system. | Export has to be deducted from regional feedstock forecasts. |

| Collision or total loss | A relatively young pack may enter auction or salvage channels early. | Early supply is real, but condition, identity, and buyer demand vary pack by pack. |

This creates a market condition that looks contradictory but is not. Recyclers can face a shortage of true aged-retirement feedstock while dismantlers hold growing inventories of crash-sourced or one-off packs. Circular Energy Storage's observed price data put average North American used EV battery prices at $44.20 per kWh in Q4 2025, down 33.3% year over year. The decline shows that available packs are not automatically liquid inventory. Their value still depends on a buyer that can use the specific pack.

Long Warranties Change The Used-Battery Sales Opportunity

Battery longevity is only half the issue. Warranty structure is the other half.

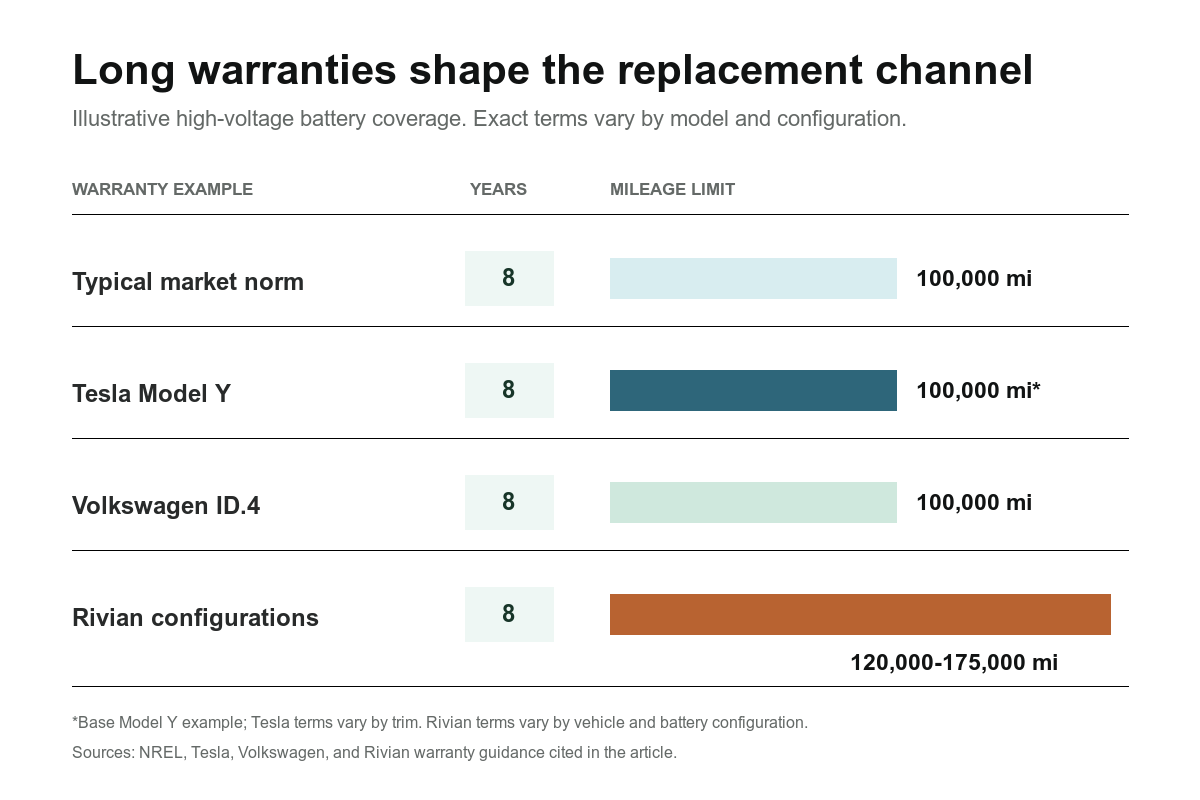

NREL's EV basics guidance describes the typical EV battery warranty as 8 years or 100,000 miles, with expected battery life often longer in moderate climates. Major OEM examples follow the same broad pattern. Tesla lists Model Y battery and drive unit coverage at 8 years or 100,000 miles. Volkswagen's U.S. ID.4 guidance also uses 8 years or 100,000 miles for the high-voltage battery. Rivian lists coverage that can run from 8 years and 120,000 miles up to 8 years and 175,000 miles, depending on configuration.

That warranty coverage creates a channel effect. If the vehicle is covered and the battery fails, the customer is not shopping for a used battery from a dismantler. The customer is taking the vehicle to an authorized service path.

Public data does not provide a clean channel-share split for failed packs by warranty status. The defensible operating assumption is narrower: covered battery failures usually begin in an authorized service path, while independent supply becomes more important as vehicles age out of warranty or arrive through collision, fleet, and salvage channels.

For salvage yards and parts sellers, this means the used-pack market is not simply "more EVs equals more used batteries." The better working model is "more identifiable, out-of-warranty, crash-sourced, fleet-sourced, or programmatic battery supply equals more opportunity."

Where Used EV Battery Supply Is More Likely To Move First

The near-term used-battery opportunity is not zero. It is concentrated.

- High-mileage fleets, taxis, rideshare, and autonomous fleets can reach service or retirement decisions earlier than consumer vehicles.

- Crash and insurance total-loss vehicles can release younger packs, but total loss does not guarantee a reusable battery.

- Out-of-warranty vehicles are more likely to enter independent repair, salvage, and used-parts channels.

- Recalls, defects, and warranty returns can create large movements, but they usually remain inside controlled programs.

- Structured remanufacturing and second-life programs can absorb identifiable, tested packs in repeatable configurations.

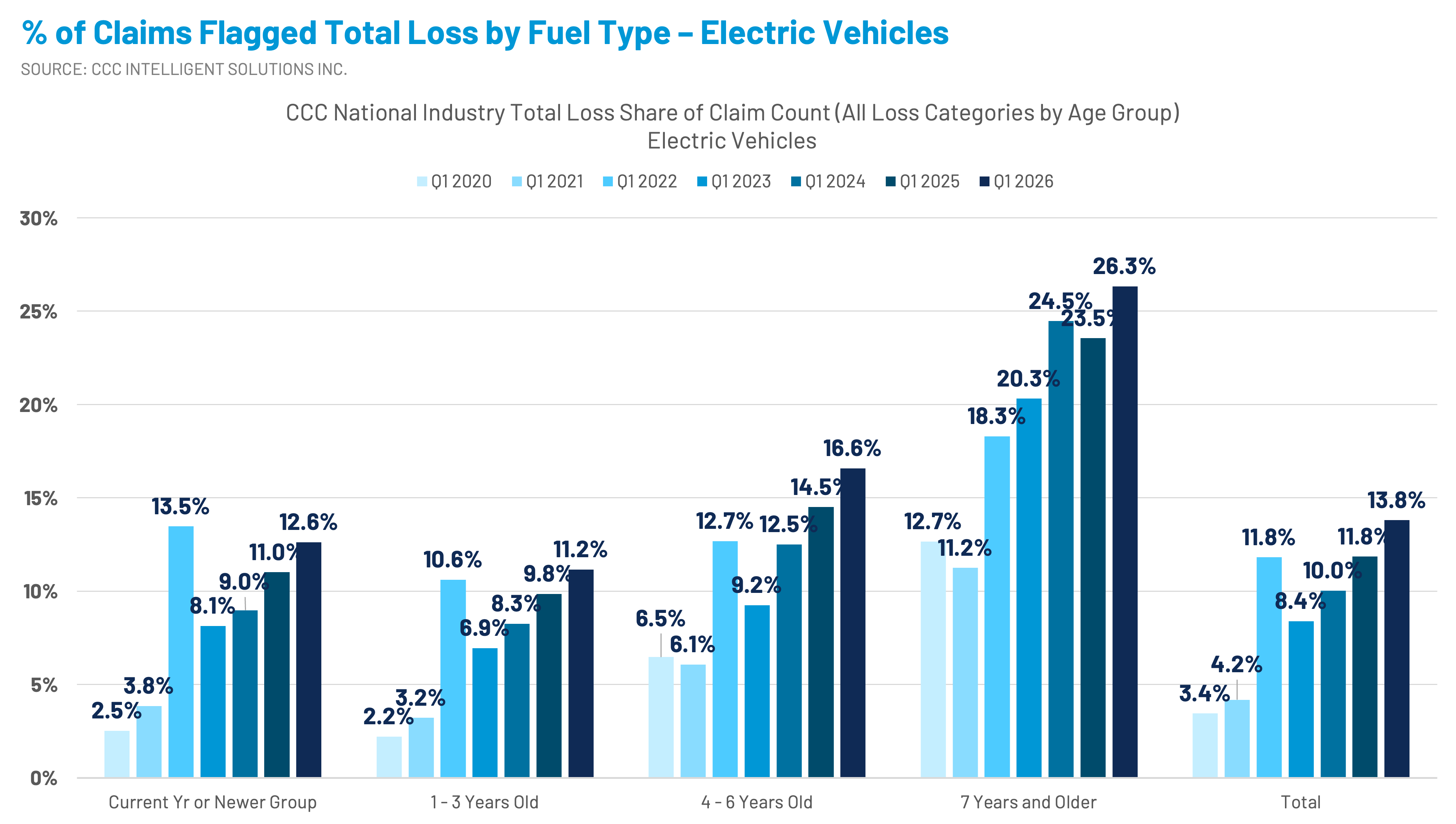

Mitchell's Q1 2026 EV collision insights show why crash and total-loss channels matter. BEVs represented 3.33% of U.S. repairable collision claims in Q1 2026, and BEV claim exposure is still rising. Collision flow is one of the more immediate ways batteries reach auctions, dismantlers, insurers, and recyclers before the aged-retirement wave matures.

This is also where EV total-loss economics connect directly to battery lifecycle value. A total-loss EV can look like a parts vehicle, a hazardous handling problem, a reusable battery asset, a recycler load, or a data problem. Without battery identity, pack condition, and routing context, the market sees less value than may actually be there.

Second-Life Buyers Need Similar Packs, Not Just More Packs

Second-life battery reuse is real, but it does not behave like a random salvage-parts market.

A second-life energy storage company needs batteries that can be tested, grouped, controlled, insured, and supported in a new application. That usually means repeatable pack families, known state of health, known chemistry, compatible form factors, and enough volume to justify engineering work.

The U.S. Department of Energy has emphasized that state of health is critical to screening, reassembly, and second-life operation. A pack with a VIN, label, chemistry, voltage, energy rating, serial context, and credible condition record is a different product than an anonymous loose battery with unknown history.

Uniform supply is necessary, but it is not sufficient. The project must also overcome testing, integration, certification, warranty, insurance, and support costs while competing with new batteries. The downstream buyer is purchasing cost-competitive function, not a used-battery identity. The strongest second-life opportunities are therefore applications where used batteries have a real cost or supply advantage.

Programs built around controlled fleets show the supply advantage. Waymo and B2U Storage Solutions are repurposing batteries from an electric autonomous fleet. Connected Energy and Forsee Power have worked with repeatable ZEN 35 and ZEN 42 electric-bus packs. Fleet, bus, taxi, and rideshare channels can eventually create more uniform batches than random consumer salvage.

Second-life buyers need a defensible evidence chain: vehicle context, pack identity, labels, photos, chemistry, fitment, and condition data. They also need that evidence to be repeatable across many batteries, not just sufficient for one correct match.

For Recyclers, The Near-Term Problem Is Feedstock Timing

For battery recyclers, the most important implication of EV battery longevity is not that recycling demand disappears. It is that the source mix may be different, and the true aged-retirement wave may arrive later.

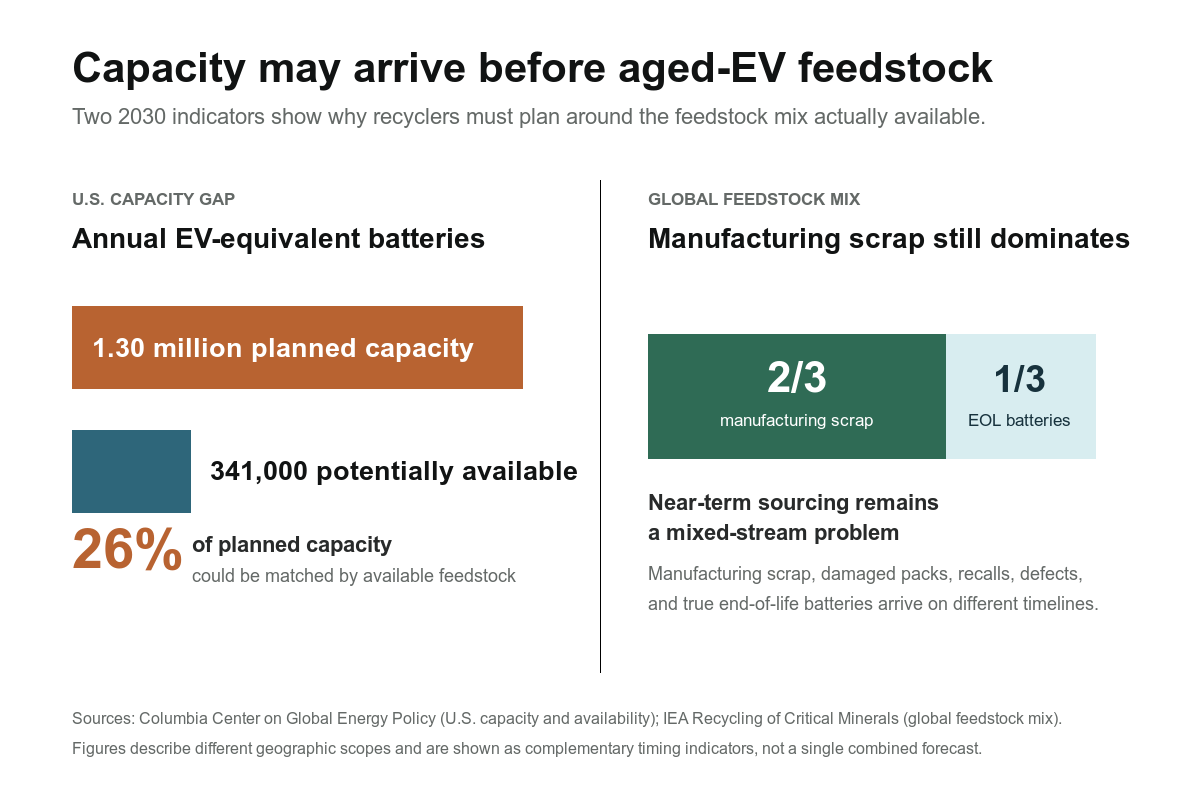

The International Energy Agency reports that manufacturing scrap still accounts for two-thirds of available recycling feedstock in 2030, with end-of-life EV and storage batteries becoming more important later. Columbia University's Center on Global Energy Policy has highlighted a similar capacity-timing issue in the U.S. market: planned recycling capacity could reach 1.3 million EV-equivalent batteries annually by 2030, while only about 341,000 EV-equivalent batteries may be available by then.

ABI Research has also estimated that around one-third of waste EV batteries in 2030 will be true end-of-life batteries from vehicles, with the rest coming from factory scrap. Before Li-Cycle entered Canadian CCAA restructuring and related U.S. Chapter 15 bankruptcy proceedings in May 2025, its 2024 annual filing described the operating reality clearly: recycler feedstock comes from a mix of battery manufacturing scrap, end-of-life batteries, damaged batteries, defective batteries, and recalled batteries.

That capacity gap makes utilization the immediate problem. Higher future volumes can spread fixed costs and improve collection and transportation efficiency, but equipment built early still has to survive the wait.

Near-term operators may therefore depend longer on manufacturing scrap, warranty returns, recalls, damaged packs, consumer lithium-ion streams, and direct sourcing relationships with fleets, auctions, dismantlers, and OEMs.

The feedstock question is not just "how many EVs are on the road?" It is:

- How old are the batteries?

- Are they still under warranty?

- Are they in OEM/dealer channels, independent salvage channels, fleet channels, or direct recycler channels?

- Are they reusable, remanufacturable, second-life eligible, or recycling-only?

- Can the pack be identified and aggregated into a useful chemistry and form-factor stream?

- Is the recycler's equipment designed for the feedstock mix that is actually available?

That is why routing intelligence matters. A recycler does not just need "batteries." A recycler needs known chemistry, safe handling context, packaging and logistics discipline, and predictable inbound streams. A second-life operator needs many of the same fields, but may route the pack differently based on state of health and pack family.

Battery Value Has A Floor And Two Ceilings

As an operating framework, recycling can be treated as the battery's value floor. The floor starts with recoverable material value, then accounts for recovery rates, preprocessing costs, competitive conditions, and recycler margin. It may be a positive payment to the owner or a gate fee the owner has to pay.

The highest ceiling is often direct automotive reuse because a verified pack is a model-specific replacement component. If that market does not exist, repurposing opens a wider buyer pool but faces a different ceiling: the delivered cost and performance of a new battery system. That is why identity, state of health, pack-family repeatability, and local buyer demand must be established before an operator assigns value.

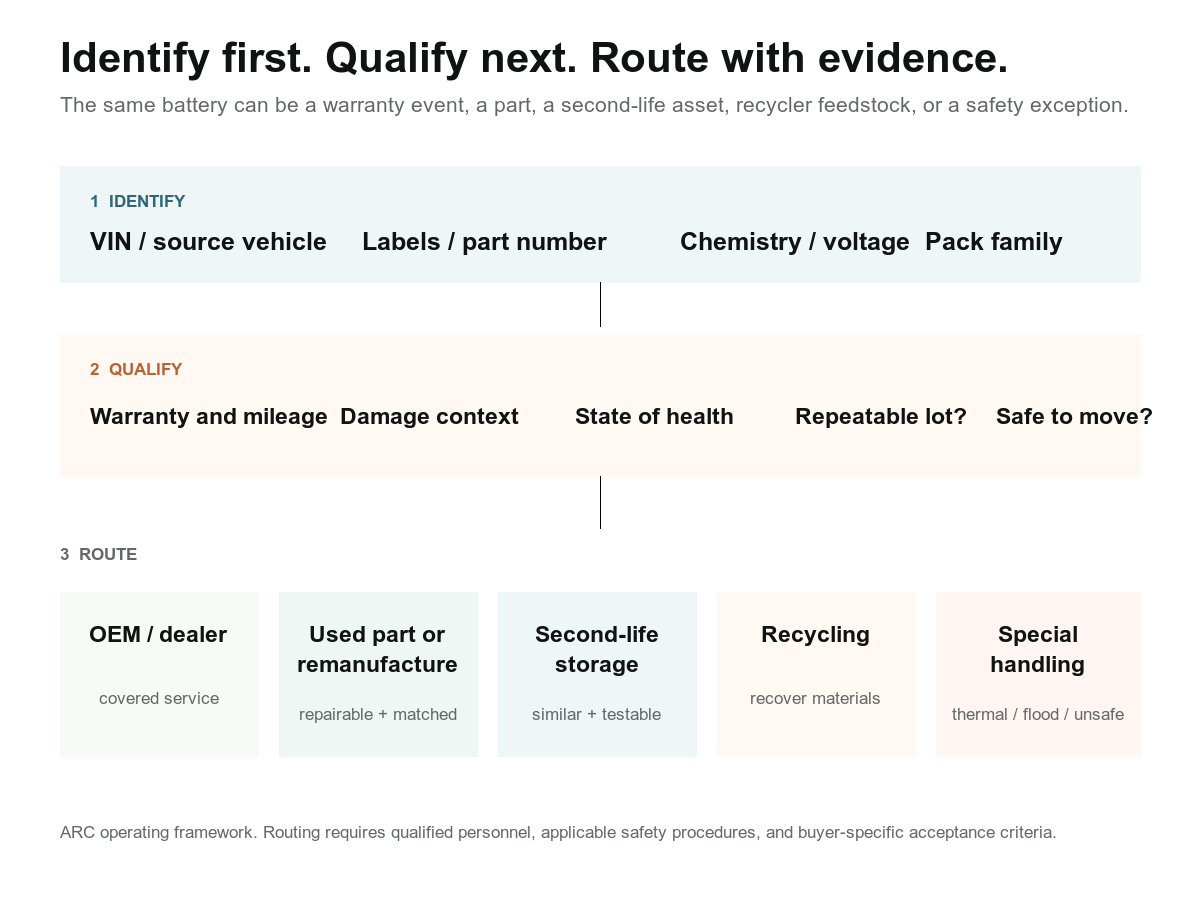

Use this routing model before pricing or moving a battery:

| Intake field | Why it matters |

|---|---|

| VIN or verified source vehicle | Narrows the pack family, model year, trim, electrification type, and possible warranty context. |

| Battery label and part number evidence | Separates service number, engineering number, assembly number, serial number, barcode, supplier, chemistry, voltage, and energy rating. |

| Warranty status and mileage | Indicates whether a failed pack should be expected to route through OEM/dealer service rather than independent used-parts channels. |

| Damage context | Collision, flood, thermal event, handling damage, recall, or normal retirement changes buyer pool and logistics requirements. |

| State of health | Determines whether the pack is repairable, reusable, second-life eligible, or recycling-only. |

| Pack family repeatability | Determines whether the battery is a one-off listing or part of a usable batch for remanufacturing or second-life storage. |

| Chemistry and form factor | Drives recycler process fit, safety handling, transportation, and buyer qualification. |

| Documentation quality | Better photos, labels, and traceability increase buyer confidence and reduce misrouting. |

This is also why battery reverse logistics has to be paired with battery intelligence. It is not enough to move a pack safely. The operator has to know what it is, where it should go, and why.

How ARC Thinks About The Market

ARC's view is that EV battery lifecycle value will be decided by evidence quality and routing discipline.

For salvage yards, the opportunity is not a generic flood of used packs. It is the ability to recognize the right packs, document them correctly, and route them to buyers that actually match their condition and configuration.

For second-life and remanufacturing buyers, the opportunity is not random supply. It is concentrated supply: high-mileage fleets, taxis, rideshare operations, buses, autonomous fleets, and battery families that can be aggregated into repeatable lots.

For recyclers, the opportunity is not just more capacity. It is feedstock access, chemistry visibility, and the ability to handle the actual source mix available today, including manufacturing scrap, recalls, damaged packs, total-loss vehicles, out-of-warranty packs, and eventually a larger wave of aged EV retirements.

ARC's Explorer is built around that operating reality. It connects vehicle context to battery pack identity, label evidence, battery specifications, cell-level context, and market routing intelligence. If your team is receiving EVs, buying battery cores, qualifying second-life supply, or building recycler feedstock programs, start with the battery identity record.

Open Explorer or review the Explorer-by-VIN API docs if you need to connect battery identity to an existing intake, auction, dismantling, or recycling workflow.

FAQ

Do EV battery warranties reduce used EV battery sales?

They can reduce broad used-pack sales while vehicles are still covered. If a battery fails under warranty, the owner is usually routed through the OEM or dealer service path for a covered repair. That limits how many warranty-age failed packs should be expected to appear as ordinary independent used-parts inventory.

Are EV batteries lasting longer than expected?

Yes, the current evidence points that way. Recurrent found low replacement rates outside major recalls, Geotab found average degradation of 2.3% per year, and Stanford/SLAC research found real-world use may extend battery life versus conventional lab assumptions.

Why is EV battery recycling feedstock arriving later than expected?

Battery durability is only one delay. Many packs remain inside their original vehicles for well over a decade, and exported vehicles carry their batteries out of the domestic collection system. Warranty channels and low replacement rates delay independent supply further.

Can used EV battery inventories grow while recycling feedstock remains tight?

Yes. Crash-sourced and one-off packs can accumulate in salvage inventory when replacement and second-life demand is thin, even while recyclers wait for larger volumes of true aged-retirement feedstock.

Where will used EV battery supply come from first?

Near-term supply is more likely to come from high-mileage fleets, taxis, rideshare, crash-total-loss vehicles, recalls, defective batteries, out-of-warranty vehicles, and structured battery programs than from a broad wave of ordinary consumer battery failures.

Bottom Line

The WSJ consumer story is that EV batteries are proving more durable than many buyers expected. The operator story is that battery durability, vehicle survival, warranty channels, exports, and weak buyer liquidity all reshape when and where feedstock appears. A shortage of aged retirement feedstock can coexist with too many hard-to-sell salvage packs.

Battery longevity does not remove the lifecycle opportunity. It makes accurate identity, condition evidence, regional flow data, and routing discipline more valuable. Before pricing or moving a pack, establish what it is, whether it is under warranty, what condition it is in, and which buyer can use it.

Sources And Further Reading

- EV Batteries Are Defying Expectations After Hundreds of Thousands of Miles, Wall Street Journal

- New Data: How Long Do Electric Car Batteries Last?, Recurrent

- EV Battery Health: What 22,700 Electric Vehicles Tell Us, Geotab

- Existing EV batteries may last up to 40% longer than expected, Stanford

- Asset or liability? The future value of used batteries, Circular Energy Storage

- The reuse pivot, the recycling stumble, and what the data actually says, Circular Energy Storage

- The Real Battery Economy, Seen Through Prices, Circular Energy Storage

- Electric Vehicle Basics, NREL

- Tesla Model Y official page

- Volkswagen EV warranty guidance

- Rivian warranty support

- Recycling of Critical Minerals, International Energy Agency

- Strengthening the US EV Battery Recycling Industry to Onshore Critical Material Supply, Columbia Center on Global Energy Policy

- US EV Battery Recycling Industry Faces Challenge as Input Supply Reaches Only a Quarter of Capacity by 2030, ABI Research

- Li-Cycle 2024 annual report, SEC filing

- Li-Cycle restructuring and bankruptcy proceedings, SEC Form 8-K

- Plugged-In: EV Collision Insights Q1 2026, Mitchell

- A second life for EV batteries, clean energy for communities, Waymo

- Recycling and Second-Use Selections Factsheets, U.S. Department of Energy

- Forsee Power and Connected Energy using second-life batteries